Liechtenstein Blockchain Act: How can nearly any right and therefore any asset be tokenized based on the Token Container Model?

In January 2020, new blockchain laws will come into force in Liechtenstein. Based on these laws, companies and entrepreneurs can tokenize any right and therefore also any asset in a straightforward way. Then, complex workarounds or far-fetched interpretations of decade-old paragraphs are not needed anymore. This will provide legal certainty and inevitably lead to the emergence of the token economy. Standardized processes and registered service providers for tokenization will be emerging in Liechtenstein. This will significantly reduce the time and cost needed for tokenization processes. Ultimately, hundreds if not thousands of tokens can be expected to be issued in Liechtenstein in 2020. What exactly will be tokenized? Almost everything.

Authors: Philipp Sandner, Thomas Nägele, Jonas Gross

The Liechtenstein Blockchain Act

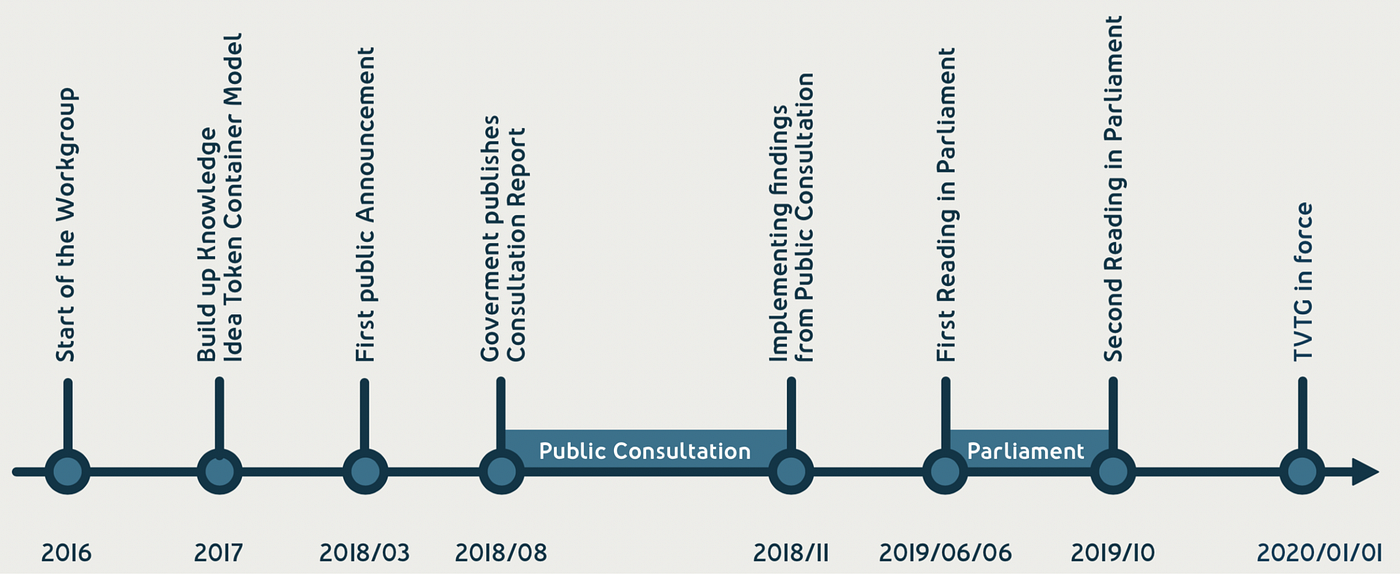

Liechtenstein did it! In the beginning of October 2019, the second hearing of the Liechtenstein Parliament on the new Liechtenstein Blockchain Act took place. No significant issues arose during this hearing. The result is that the Liechtenstein Blockchain Act will come into force in January 2020 and allows straightforward tokenization of all kinds of assets and rights without legal workarounds (see Figure 1).

Precisely, the Liechtenstein Blockchain Act is actually called “Tokens and TT Service Providers Law” (TVTG) but we will, for the remainder of this article, use the former expression. Also, the new law uses the generic word “trustworthy technology” (TT) which can include blockchain and DLT systems. Please note that for easier readability we simply use the word “blockchain”.

The Liechtenstein Blockchain Act is a collection of new rules and changes of existing laws that allow rights and assets to become tokenized. Tokenization means that as of January 2020 nearly any right or asset can be “packaged” into a token according to the Token Container Model. Liechtenstein thereby acknowledges that — driven by digital transformation — the physical world as we know it for hundreds of years will sooner or later be augmented by a digital world.

Often, we use paper documents to agree on a contract or for proofing evidence. This contracts then “creates” rights for the involved parties. Notaries are responsible to print, read and verify identities and documents — mostly all processes are conducted on paper. The Liechtenstein Blockchain Act now acknowledges that such paper-based rights and assets (yes, they can also be written on a PDF-document and signed digitally) can and will be brought to the digital world and will become tradeable easily: in the form of tokens. If thousands of rights and assets will be represented by digital tokens in a couple of years, we suddenly have two worlds: (1) the physical world as we know it and (2) the new digital world, which includes a subset of the rights and assets of the physical world. To become practical: But who is actually owning my house? The person in the real estate register? Or the person owning the token? What if the token is being stolen, or lost?

The Liechtenstein Blockchain Act also integrates the fact that the physical world always needs to be in perfect synchrony with the digital world of the tokens. This is very important because tokens can be, for example, lost or stolen. Also for this reason, Liechtenstein amended the civil law which is truly fascinating. This, by the way, is one fact that makes the Liechtenstein Blockchain Act really outstanding and in our mind a best-in-class framework.

The Token Container Model

One of the building blocks of the Liechtenstein Blockchain Act is the so-called Token Container Model (TCM). With this framework, a token serves as a container with the ability to hold rights of all kinds. The container can be “loaded” with a right that represents a real asset such as real estate, stocks, bonds, gold, access rights, money. But the container can also be empty. The latter case applies for example to digital code — the most notable example being Bitcoin.

This approach of loading a right or asset into a container (i.e., into a token) may sound trivial but allows a separation of (1) the right and the asset on the one hand side and (2) the token technically “running” on a blockchain-based system on the other hand side. In this manner, Liechtenstein differentiates between (1) law and (2) technology.

Therefore, this model is truly helpful to understand the process and the impact of tokenization. All rules governing the right and the asset basically stay as they are. But some specific rights are changed through the digital nature of the right packaged into a token. Here is an example: Some people think that security tokens (i.e., a stock on a blockchain system) are a new class of securities. But the Token Container Model makes very clear that a security token is nothing else than a security (with all the rules, licenses, duties etc. applying to it) technically “packaged” into the token which loads the security like a container. The word “container” is meant literally. The token can now be transferred to new owners, can be managed in a portfolio or can safely be stored by a custody provider — without the right and asset within the container changing.

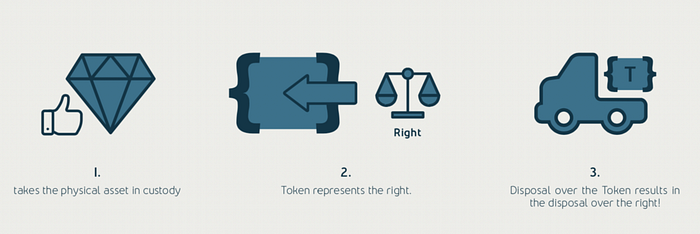

To illustrate this for clarity: A right is virtually stored in a container (see panel 2, Figure 2) representing the token and running on a blockchain-based system. The right could, for example, be the ownership right of a diamond (see panel 1, Figure 2). Whoever owns the token owns the diamond — exactly this relation is established by the Token Container Model. The diamond does not need to move its physical location; it can remain in a vault. But the ownership of the diamond can change by transferring the token to other persons (see panel 3, Figure 2). This would make sense for a private person storing value by owning a diamond but also for institutional investors who build entire portfolios of fractionally owned diamonds (think of 1,000 investments in fractions of a diamond for the purpose of risk diversification).

This model is progressive and provides legal certainty for pre-existing rights that are tokenized as well as for the information stored on blockchain-based systems. Note that Liechtenstein amended its civil law to allow the token world to have priority over the physical world for the cases where tokens exist for rights and assets.

The physical validator has the duty to integrate the physical with the digital world

One guiding principle of the Liechtenstein Blockchain Act is that some new service providers that interact with the blockchain and the tokens need to be regulated. Some of these new formats of service providers need not only a registration with the Liechtenstein Financial Market Authority (FMA), but also a license to operate. One of these new roles is the so-called physical validator. His role is to integrate the physical world into the digital world.

The physical validator has the duty to identify the holder of the tokens. In the previous example with the tokenized diamond (Figure 2), the physical validator knows who is owning the token and, with it, the diamond and has the duty to ensure the contractual enforcement of the represented rights and obligations, e.g. by storing the assets (or rights) of the real world in a vault. This is done by the physical validator. He also has the responsibility for having established correct business processes. If errors occur, if the physical assets are stolen or damaged, or if he does not comply with the rules, it is his responsibility to solve these issues. If he is not capable to do so, he risks his licence as a service provider and therefore loses the right to operate. With this approach, the Liechtenstein Blockchain Act assigns the responsibility to guarantee a perfect synchrony of the physical world and the digital world to the physical validator. Therefore, the newly defined role of the physical validator is highly important as it enables the token economy: providing certainty and allowing the tokenization of an existing right and its subsequent valid transfer onto a blockchain system.

Tokenization of any right and asset

According to the Token Container Model, any asset or right can basically be represented by a token. Some examples can be seen in Figure 3. For example, a software license right or an access right can be put into the token container. In most jurisdictions this would be classified as a utility token. If the token is sold to the market before the development of the product has actually been finished, this process is called Initial Coin Offering (ICO).

Next, applying the European E-Money framework would allow to package traditional currencies such as the Euro or the Swiss Franc into a token. These tokens would be classified as payment tokens, more precisely, Euro tokens, digital Euro, Euro on blockchain, cash on ledger, etc. This is nothing else than putting a Euro into a token by applying E-Money rules for the content of the container.

Ultimately, a security can packaged into the token. Then, all securities’ laws apply and the result is a security token. If sold to investors, we call this process a Security Token Offering (STO).

Tokenization follows a life cycle

When a right or an asset is tokenized, first, the tokens need to be generated technically. Then, the tokens need to be issued to the new holders. This can take place in a token sale (e.g. STO, IEO, ICO). Tokens then can be traded against other tokens and in most cases they need to be custodied. Even more so, tokens — in the financial market — can be purchased and placed in a portfolio for investing purposes etc.

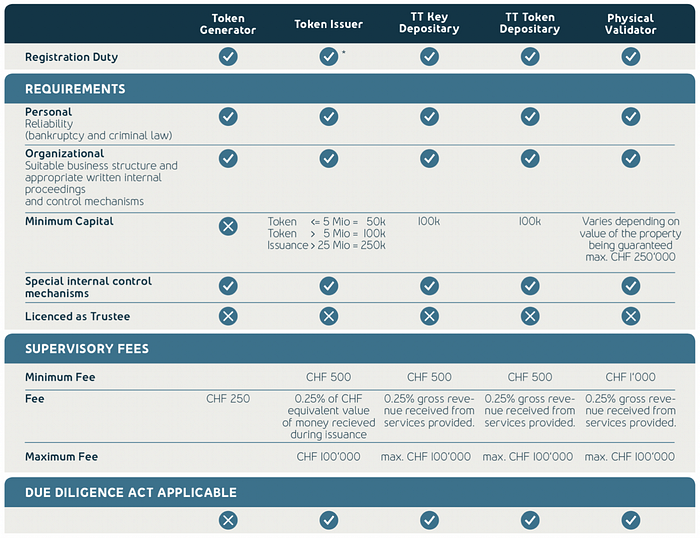

To put it in a nutshell, tokens have a life cycle. Different events in the life cycle of the token indicate different requirements of the actors, e.g. token generator, token issuer, token depositary. The Liechtenstein Blockchain Act therefore provides multiple possibilities to register with the FMA such that companies can act along the life cycle of tokens. As Figure 4 points out, companies can soon apply for these registrations. There are multiple requirements for the applicant. And, of course, licenses are not for free. But comparing the fees and requirements for other registrations or licenses of financial authorities indicate that fees for licenses in Liechtenstein are reasonable. Once clearly defined registrations exist, as is the case in Liechtenstein, and once tokenization processes and smart contracts become standardized, ultimately costs for tokenization of any asset will be brought down.

Liechtenstein and other countries

Liechtenstein sets forth a technologically neutral and all-encompassing framework designed to capture all aspects of tokenization. Due to Liechtenstein’s status as a member of the European Economic Association (EEA), compliance with codified EU/EEA guidelines and regulations is required. These base line regulations create a floor that Liechtenstein legislators are able to build upon. The registrations and licences issued under the foundational regulations and directives of the EU/EEA are passportable to other EU/EEA member states, while the Liechtenstein unique registrations under the Blockchain Act are not passportable. Of course, tax regulations in other countries and also the upcoming “crypto license” in Germany might make business endeavors here and there more complex but not unfeasible.

At the core, the Liechtenstein Blockchain Act is focused on adapting pre-existing laws to foster legal certainty within the token economy. Drawing a clear line between what falls under civil law versus regulatory and supervisory law, the Liechtenstein Blockchain Act includes changes of the Liechtenstein Persons and Companies Act, Trade Act, Due Diligence Act, and Financial Market Authority Act. Probably the most important aspect are the changes in the civil right, to ensure that the underlying right represented by the token is effectively transferred from party A to party B. Besides this, the act provides regulatory and supervisory rules regarding those interacting with blockchain systems — including consumers, service providers, and intermediaries.

Liechtenstein: “straightforward tokenization” without workarounds

In case you try to tokenize rights and assets, this is typically difficult and challenging with local laws in place. In Germany for example, specific forms of debt can be tokenized but no shares or bonds up to now. A skilled lawyer is always necessary trying to find a workaround and — subsequently — convincing the regulatory bodies that the proposed workaround is complying with the local law by interpreting some paragraph of the law in a “new” way. The lawyer of course would never call this workaround a workaround. Nevertheless, it is often possible but not easy. Typically, such workarounds are also expensive since they are not yet subject to a standardized process.

Therefore, Liechtenstein will be an interesting destination for various tokenization efforts: Without time-consuming and costly efforts, rights and assets can be tokenized in a straightforward way. No workarounds are required as in other countries. This will not only standardize processes but will also decrease costs for tokenization processes significantly.

Ultimately, for 2020 we can expect that hundreds if not even thousands of assets or rights will be tokenized in Liechtenstein. Some of them will be publicly announced as security tokens but the majority of tokens will be created for direct relationships (e.g. private placements during fundraising) or B2B purposes.

Remarks

In Germany, regulatory changes for companies dealing with crypto assets are ahead. As follows, read about Germany’s national blockchain strategy and the upcoming “crypto license” required in Germany for all companies that handle crypto assets:

The full version of the Liechtenstein Blockchain Act, or “Tokens and TT Service Providers Law” (TVTG) in German as well as the English-translated Government Consultation Report is available here:

- English version: https://nlaw.li/tvtgen

- German version: https://nlaw.li/tvtgde

If you like this article, we would be happy if you forward it to your colleagues or share it on social networks. If you are an expert in the field and want to criticize or endorse the article or some of its parts, feel free to leave a private note here or contextually and we will respond or address.

Do you want to learn more about how blockchain will change our world?

- Blockchain knowledge: We wrote a Medium article on how to acquire the necessary blockchain knowledge within a workload of 10 working days.

- Our two blockchain books: We have edited two books on how blockchain will change our society (Amazon link) in general and the everything related to finance (Amazon link) in particular. Both books are available in print and for Kindle — currently in German and soon in English. The authors have been more than 20 well-known blockchain experts in startups, corporations and the government from Germany, Austria, Switzerland and Liechtenstein — all contributing their expertise to these two books.

Authors

Thomas Naegele advises international finance, technology and industrial enterprises, operating in the fields of Blockchain/DLT, telecommunications and Internet, as well as public institutions. As a Liechtenstein attorney and being an experienced software developer, he focuses on Internet/IT law, as well as civil and corporate law. Besides being an attorney and legal advisor, he teaches at the University of Liechtenstein and gives lectures and presentations on the newest legal developments. You can reach him via LinkedIn (https://www.linkedin.com/in/thomasnaegele/).

Prof. Dr. Philipp Sandner has founded the Frankfurt School Blockchain Center (FSBC). From 2018 to 2021, he was ranked among the “top 30” economists by the Frankfurter Allgemeine Zeitung (FAZ), a major newspaper in Germany. He has been a member of the FinTech Council and the Digital Finance Forum of the Federal Ministry of Finance in Germany. He is also on the Board of Directors of FiveT Fintech Fund and Blockchain Founders Group — companies active in the field of blockchain startups. The expertise of Prof. Sandner includes crypto assets such as Bitcoin and Ethereum, decentralized finance (DeFi), the digital euro, tokenization of assets, and digital identity. You can contact him via mail (m@philippsandner.de) via LinkedIn or follow him on Twitter (@philippsandner).

Jonas Gross is project manager and research assistant of the Frankfurt School Blockchain Center (FSBC). His fields of interests are primarily security tokens. Besides, in the context of his PhD he analyzes the impact of blockchain technology on monetary policy of worldwide central banks. He mainly studies innovations as central bank digital currencies (CBDC) and central bank crypto currencies (CBCC). You can contact him via mail (jonas.gross@fs-blockchain.de), LinkedIn (https://www.linkedin.com/in/jonasgross94/) and via Xing (https://www.xing.com/profile/Jonas_Gross4).